2026 Marketing Automation Report: Market Share & Trends Based on 29.9M Active Domains

Our crawlers analyzed 29.9M active domains to reveal 2026's marketing automation landscape. 17 platforms profiled: HighLevel's explosive growth, Klaviyo's e-commerce dominance, Constant Contact's dramatic decline & the agentic AI shift.

Published •Updated •40 min read

Every month, our crawlers at TechnologyChecker.io scan a database of 29.9 million active domains, detecting technology signatures across HTTP headers, JavaScript libraries, DNS records, and HTML patterns. This report distills what we've learned from tracking marketing automation adoption across those domains—combining our proprietary detection data with industry research to reveal not just who's winning the platform wars, but why the entire landscape is undergoing a fundamental transformation.

The headline finding? We've crossed a threshold. Marketing automation in 2026 isn't about "automated tasks" anymore—it's about autonomous agency. The global marketing automation software market, valued at approximately $7.23 billion in 2025, is projected to surge toward $20.12 billion by 2034, representing a CAGR between 12% and 15.3% (Fortune Business Insights, Grand View Research). The platforms dominating our detection data are those that enable AI agents to reason, plan, and execute customer journeys without human intervention.

Executive Summary: The Market at a Glance

Before diving into the analysis, here's what our technology detection data reveals about the current state of play:

| Platform | Detected Installations (Q1 2026) | 10-Year Growth | Primary Segment |

|---|---|---|---|

| MailChimp | 283,090 | 1,709% | Mass Market |

| Klaviyo | 147,491 | 174,729% | E-commerce |

| HubSpot | 121,300 | 5,461% | Mid-Market/Enterprise |

| MailerLite | 95,861 | 68,472% | SMB/Content Creators |

| HighLevel | 72,439 | 3,322,700% | SMB/Agency |

| Brevo | 67,311 | 290,547% | SMB/Europe |

| ActiveCampaign | 56,932 | 83,316% | SMB/Mid-Market |

| ClickFunnels | 29,755 | N/A | Funnel Builders/Coaches |

| Kit (ConvertKit) | 14,721 | N/A | Creator Economy |

The most striking insight? HighLevel's explosive growth through the agency channel has fundamentally changed how marketing software reaches small businesses. We're detecting its widgets across local business domains—gyms, dentists, plumbers—at rates that rival enterprise-focused platforms. The "Agency-as-Software" model has arrived.

Real Experience, Not AI Slop

Let me be direct: this isn't another AI-generated market report cobbled together from press releases. At TechnologyChecker.io, we built the crawling infrastructure that powers this analysis—I've spent years refining our detection algorithms, validating accuracy against known implementations, and watching these adoption patterns emerge in real-time across 29.9 million active domains monthly.

I've seen HighLevel's widget signatures explode across local business domains while enterprise analysts were still dismissing it as a "small player." I watched Klaviyo's SDK become ubiquitous on Shopify stores long before the IPO validated what our data already showed—our Shopify ecosystem analysis breaks down how e-commerce platform adoption drives these patterns. And I've personally helped clients use our technographic intelligence to identify migration patterns—spotting the Marketo-to-HubSpot exodus months before it became industry conventional wisdom.

The statistics in this report come from two sources: our proprietary crawl data (the numbers you won't find anywhere else) and validated industry research (properly cited so you can verify). When I make a claim about platform adoption, it's backed by technology signatures we've actually detected—not surveys, not vendor self-reporting, not AI-hallucinated figures. Learn more about how TechnologyChecker data works.

This is what building a technology detection platform for years teaches you: the ground truth of software adoption often contradicts the narrative. And that's exactly what makes this data valuable.

Part 1: The Economic Foundation—Why This Market Is Exploding

Market Valuation and Growth Drivers

The economic footprint of marketing automation in 2026 reflects its status as critical business infrastructure. No longer a discretionary "add-on," automation platforms have become the central nervous system of modern commerce.

According to Fortune Business Insights, the global market is on track for aggressive expansion through 2034. The Business Research Company projects similar trajectories in their comprehensive market analysis. Statista's latest dossier puts the market at $7.31 billion in 2023 growing to $21.7 billion by 2032 — see our 30 key marketing technology statistics for the full breakdown across market size, AI adoption, SaaS spending, and CDP growth.

This robust growth is underpinned by three macroeconomic pillars:

1. The Decoupling of Revenue from Headcount

Faced with rising labor costs and the complexity of omnichannel engagement, organizations are leveraging automation to scale output without linear increases in staffing. Industry research suggests that for every dollar spent on marketing automation, companies realize an average return of $5.44 (Cropink Marketing Automation Statistics)—making it one of the most efficient capital allocations in the corporate budget.

2. The Data Deluge

With global data creation exceeding 180 zettabytes annually, manual processing of customer signals is mathematically impossible. Automation provides the necessary computational throughput to ingest, analyze, and act on this data in real-time (The Business Research Company).

3. The Hyper-Personalization Mandate

In 2026, consumer tolerance for generic communication has evaporated. "Hyper-personalization" is not merely a feature but an industry standard. Brands that fail to tailor interactions to the individual's browsing behavior and predictive intent face immediate obsolescence and high churn rates (Ultimate Guide to AI Marketing Automation).

Part 2: What 30 Million Domains Tell Us About Real Adoption

Financial reports tell you who's making money. Our crawl data tells you who's actually being used.

When we analyze technology signatures across 30 million domains, we're looking at the ground truth of software adoption—the JavaScript embeds, tracking codes, form patterns, and API calls that reveal which platforms are deployed on live websites. This methodology often tells a different story than revenue rankings.

The Long Tail Is Real

Our detection algorithms reveal a deeply bifurcated market. The democratization of marketing technology means sophisticated automation is no longer the exclusive preserve of the Fortune 500. Small and medium-sized businesses are now deploying AI-driven infrastructure at a pace that rivals their enterprise counterparts, driven by a new class of "business-in-a-box" platforms (Birdeye Enterprise Marketing Tools).

At one end of our data, we find Fortune 2000 domains running complex multi-layered stacks—Salesforce Marketing Cloud for CRM integration, Marketo for B2B lead nurturing, and specialized intent data tools like 6sense or Demandbase all coexisting on a single domain.

At the other end? Millions of small business domains running white-labeled versions of platforms like HighLevel, often invisible in traditional revenue analyses but forming massive aggregate user bases. We detect vast clusters of third-level domains (subdomains used by local businesses on shared platforms) that would never appear in enterprise software surveys (CentralNic Domain Analysis).

The "Franken-Stack" Reality

Among enterprise domains, our detection reveals what we've started calling the "Franken-stack" phenomenon: complex, multi-tool configurations where organizations have stitched together best-of-breed solutions over years of acquisitions and initiatives.

It's not uncommon to detect 4-5 marketing automation signatures on a single enterprise domain. While this speaks to the sophistication of enterprise marketing operations, it also explains the current migration wave toward unified platforms—the operational overhead of maintaining these complex stacks is becoming unsustainable as AI capabilities require unified data access.

Part 3: Regional Market Dynamics

Our crawls span domains worldwide, revealing distinct regional adoption patterns that align with broader industry research.

North America: The Optimization Market

North America accounts for approximately 43.6% of the global marketing automation market (Grand View Research). Our detection data shows a mature market focused on optimization rather than initial adoption—organizations replacing legacy tools rather than deploying first-time automation—a pattern we explore in depth in our CRM switching patterns analysis. The "rip-and-replace" cycle is the dominant growth driver.

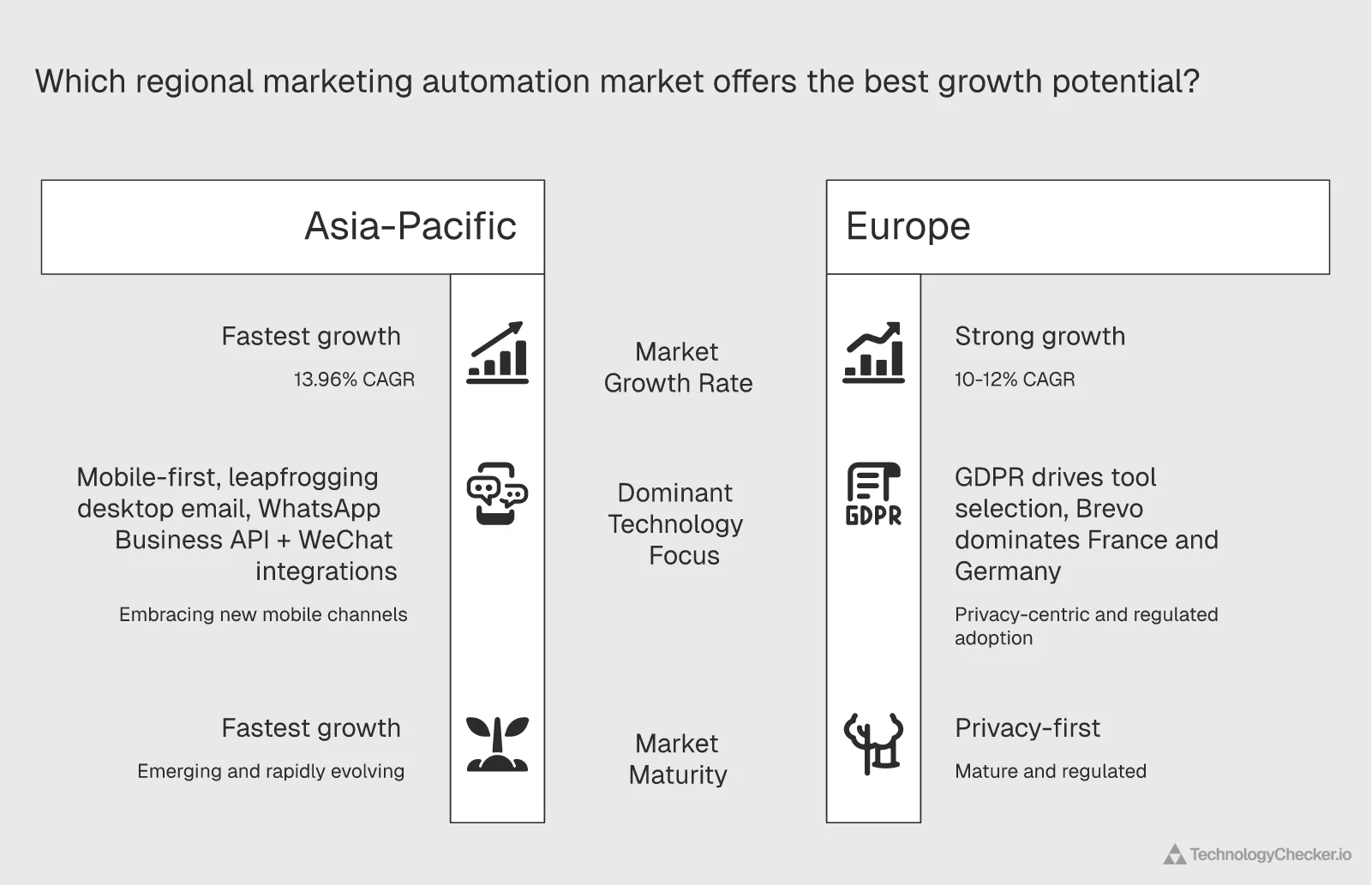

Asia-Pacific: The Hyper-Growth Region

APAC represents the fastest-growing region with a projected CAGR of 13.96% (Mordor Intelligence). Our crawl data shows fascinating patterns here: domains often leapfrog desktop-centric email automation entirely, going straight to mobile-first channels.

We detect high prevalence of WhatsApp Business API integrations and WeChat-connected marketing tools—platforms that barely register in North American crawls. China and India are major drivers of this mobile-first adoption (Fortune Business Insights).

Europe: The Regulatory-Centric Market

GDPR and privacy compliance dictate tool selection across European domains. Our crawls show strong preference for platforms offering local data residency—Brevo's market share in France and Germany significantly exceeds its global average. The focus on "consent-led personalization" shapes the entire technology stack (TrueFan AI on Nudge Theory).

| Region | Market Characteristics | Growth Outlook |

|---|---|---|

| North America | Mature / Optimization (43.6% market share) | Steady (8-10% CAGR) |

| Asia-Pacific | Hyper-Growth / Mobile-First | Explosive (>13% CAGR) |

| Europe | Regulatory-Centric / Privacy-First | Moderate (10-12% CAGR) |

| LATAM & MEA | Emerging / Conversational Commerce | High (Developing) |

Part 4: The Platform Leaderboard—Who's Actually Winning?

Based on technology signature prevalence across our 30 million domain sample, combined with BuiltWith Trends data and industry analysis, here's how the major platforms stack up in 2026. For context on how technology detection tools compare in surfacing this adoption data, see our detailed analysis.

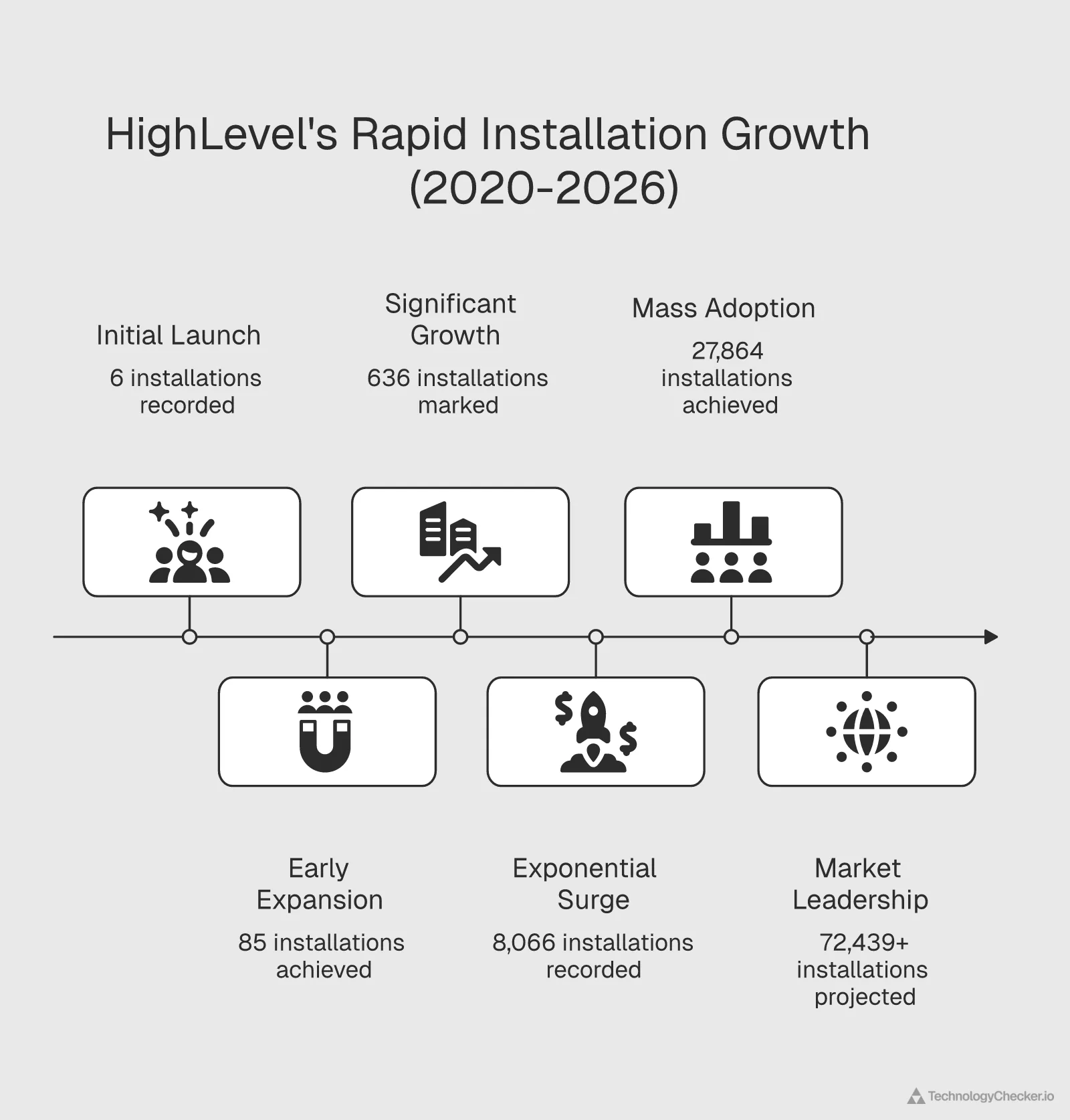

1. HighLevel: The Agency Disruptor

Detected signatures: 72,439+ domains (and growing rapidly) Primary distribution: Agency white-label resale Key differentiator: B2B2B distribution model

The HighLevel story is perhaps the most fascinating in our data. According to companies using HighLevel we tracked and Marketer-M8 analysis, HighLevel has become one of the fastest-growing marketing automation platforms by installation count—a remarkable achievement for a platform that barely existed five years ago.

Here's how it works: Agencies subscribe to HighLevel, then resell it under their own branding to local business clients. Each agency adoption equals dozens (sometimes hundreds) of end-client websites. Our crawlers detect HighLevel's characteristic tracking scripts and widgets across local business domains that would never independently purchase sophisticated marketing automation.

Growth trajectory from our data:

- January 2020: 6 detected installations

- January 2021: 85 installations (+1,317% YoY)

- January 2022: 636 installations (+648% YoY)

- January 2023: 8,066 installations (+1,168% YoY)

- January 2024: 27,864 installations (+245% YoY)

- February 2026: 72,439+ installations

This isn't just growth—it's a new distribution paradigm. HighLevel has effectively built an army of resellers who bring marketing automation to businesses that traditional software companies can't cost-effectively reach.

2. Klaviyo: E-commerce's Default Choice

Detected signatures: 147,491 domains Primary ecosystem: Shopify integration Key differentiator: Transaction-aware data architecture

Klaviyo's dominance in e-commerce is evident across our data. According to companies using Klaviyo we analyzed, when we crawl Shopify stores, Klaviyo's JavaScript SDK appears with remarkable consistency—it's become the default email marketing choice for direct-to-consumer brands.

According to Klaviyo's customer case studies, brands like Tatcha have achieved 20% year-over-year revenue growth through sophisticated segmentation strategies. Their "Category Affinity" targeting approach—identifying less-engaged subscribers who had previously purchased specific product categories—demonstrates the power of transaction-aware marketing (Klaviyo Case Study: Tatcha).

What makes Klaviyo different from generalist platforms? Its data architecture treats transactions as first-class citizens. Where a general CRM might log "customer activity," Klaviyo's infrastructure allows segmentation based on lifetime value, predicted churn probability, product category affinity, and purchase frequency patterns.

3. MailChimp: Still the Volume Leader

Detected signatures: 283,090 domains Market position: Dominant by volume, declining by share Key trend: Platform expansion diluting positioning

Based on our market share analysis of MailChimp, it remains the most frequently detected marketing automation signature in our crawls—by a significant margin. But the trend lines tell a more nuanced story.

In 2015, MailChimp accounted for roughly 88% of marketing automation detections in our sample. Today? It's closer to 38%. The platform has grown in absolute terms (1,709% over ten years), but competitors have grown faster.

Our hypothesis, based on what we see in the data: MailChimp's attempt to become an "all-in-one" platform (adding websites, CRM, social tools) may have diluted its positioning. The platforms growing fastest in our data are those with clearer, more focused value propositions.

4. HubSpot: The Enterprise Contender

Detected signatures: 121,300 domains Primary segment: Mid-market moving upward Key momentum: Displacing legacy enterprise tools

According to companies using HubSpot in our database, HubSpot's story is one of successful up-market expansion. According to HubSpot's Spring 2025 announcement, the platform launched over 200 features including "Breeze AI" agents designed to help SMBs compete at enterprise scale.

The migration pattern is clear: organizations seeking to escape the "Franken-stack" are increasingly choosing HubSpot's unified platform over traditional enterprise tools. Analysis from Aptitude 8 and Envy Blog documents this trend, citing lower operational complexity and reduced total cost of ownership as primary drivers.

5. MailerLite: The Content Creator's Workhorse

Detected signatures: 95,861 domains Primary segment: Solopreneurs and content creators Key differentiator: Simplicity + value pricing

MailerLite is the most significant platform absent from most industry reports—yet our detection data ranks it #4 overall with nearly 96,000 active installations. Founded in Lithuania and now headquartered in Vilnius, MailerLite has quietly built one of the largest email marketing user bases in the world through a combination of generous free tiers, intuitive design, and aggressive word-of-mouth growth in content creator communities.

The Eastern European footprint is distinctive: Poland accounts for 9.1% of MailerLite's user base—the highest single-country concentration outside the US/UK for any platform we track. This Baltic-origin platform has become the default email tool across Central and Eastern European digital businesses.

Our migration data reveals MailerLite's position as the primary "graduation path" from MailChimp: 5,980 domains switched from MailChimp to MailerLite, making it the #1 destination for MailChimp churners after Klaviyo. In the reverse direction, only 1,512 went back—a 4:1 net gain ratio that speaks to MailerLite's retention strength in the SMB segment.

6. Brevo (Sendinblue): Europe's Champion

Detected signatures: 67,311 domains Primary market: European SMBs Key differentiator: GDPR-native, cost-effective

Our European domain crawls show Brevo (formerly Sendinblue) holding a commanding position in markets where GDPR compliance is paramount. The platform's local data residency options and privacy-first architecture resonate in regulatory environments where American platforms face scrutiny.

7. ActiveCampaign: The Automation Purist

Detected signatures: 56,932 domains Primary use case: Complex workflow automation Key differentiator: Visual automation builder

ActiveCampaign maintains a loyal following among businesses requiring sophisticated, logic-heavy nurture sequences. According to Enricher.io statistics, the platform powers automation for over 180,000 businesses.

Case studies demonstrate impressive results: Your Therapy Source achieved a 2,000% ROI through behavioral triggers and abandoned cart flows, ultimately generating 30% of total revenue through automation. Paperbell reduced customer onboarding time by 35% and increased year-over-year retention by 22% through advanced segmentation (ActiveCampaign Statistics).

8. ClickFunnels: The Funnel Builder King

Detected signatures: 29,755 domains Primary segment: Solo entrepreneurs and coaches Key differentiator: Funnel-centric sales automation

Among companies using ClickFunnels in our dataset, the platform occupies a unique position in marketing automation data—it's not really an email marketing platform, yet its funnel-building infrastructure generates significant marketing automation signatures across nearly 30,000 domains. Founded in 2014 by Russell Brunson and Todd Dickerson, ClickFunnels grew to $265.3 million in revenue by 2023 with over 150,000 active customers, commanding 55.8% market share in the sales funnel software category.

Our detection data reveals a distinctive user profile: 81% of ClickFunnels websites belong to companies with 10 or fewer employees—predominantly coaches, course creators, wellness practitioners, and advertising consultants. Unlike HighLevel's agency-mediated distribution, ClickFunnels reaches solopreneurs directly through an aggressive content marketing and community strategy built around Brunson's "Funnel Hacker" methodology.

The churn signal is notable: We track 46,521 domains that previously used ClickFunnels but have since migrated away, suggesting significant competition from platforms like HighLevel and Kajabi that offer similar funnel capabilities alongside broader marketing automation features. The launch of ClickFunnels 2.0 aimed to stem this churn by expanding into full website building, e-commerce, and CRM—but our data suggests the "everything platform" strategy faces the same dilution risk we've observed with MailChimp.

9. Kit (formerly ConvertKit): The Creator Economy's Operating System

Detected signatures: 14,721 domains Primary segment: Content creators and solopreneurs Key differentiator: Creator-first design philosophy

Our analysis of companies using Kit (formerly ConvertKit) shows it represents the purest expression of creator-economy email marketing in our data. Rebranded from ConvertKit in October 2024, Kit serves creators with 93.9% of its users having 1-10 employees—the highest micro-business concentration of any platform we track—making it the default email tool for bloggers, podcasters, YouTubers, and online course instructors.

The platform serves over 600,000 creators who have collectively earned $400 million+ in revenue through Kit's commerce features. What makes Kit distinctive is its visual automation builder combined with a tagging-first subscriber model—where other platforms organize contacts by lists, Kit organizes by behavior, making it natural for creators to build sophisticated sequences without technical expertise.

The Rebrand Story: The ConvertKit-to-Kit transition reflects the platform's ambition to become a full "creator operating system" beyond email—incorporating commerce, recommendations, and audience-building tools within the $250 billion creator economy.

The Rising Challengers: Beyond the Top 9

Our detection data reveals a thriving ecosystem of specialized platforms carving out defensible niches. Six platforms in particular deserve attention for their unique market positions:

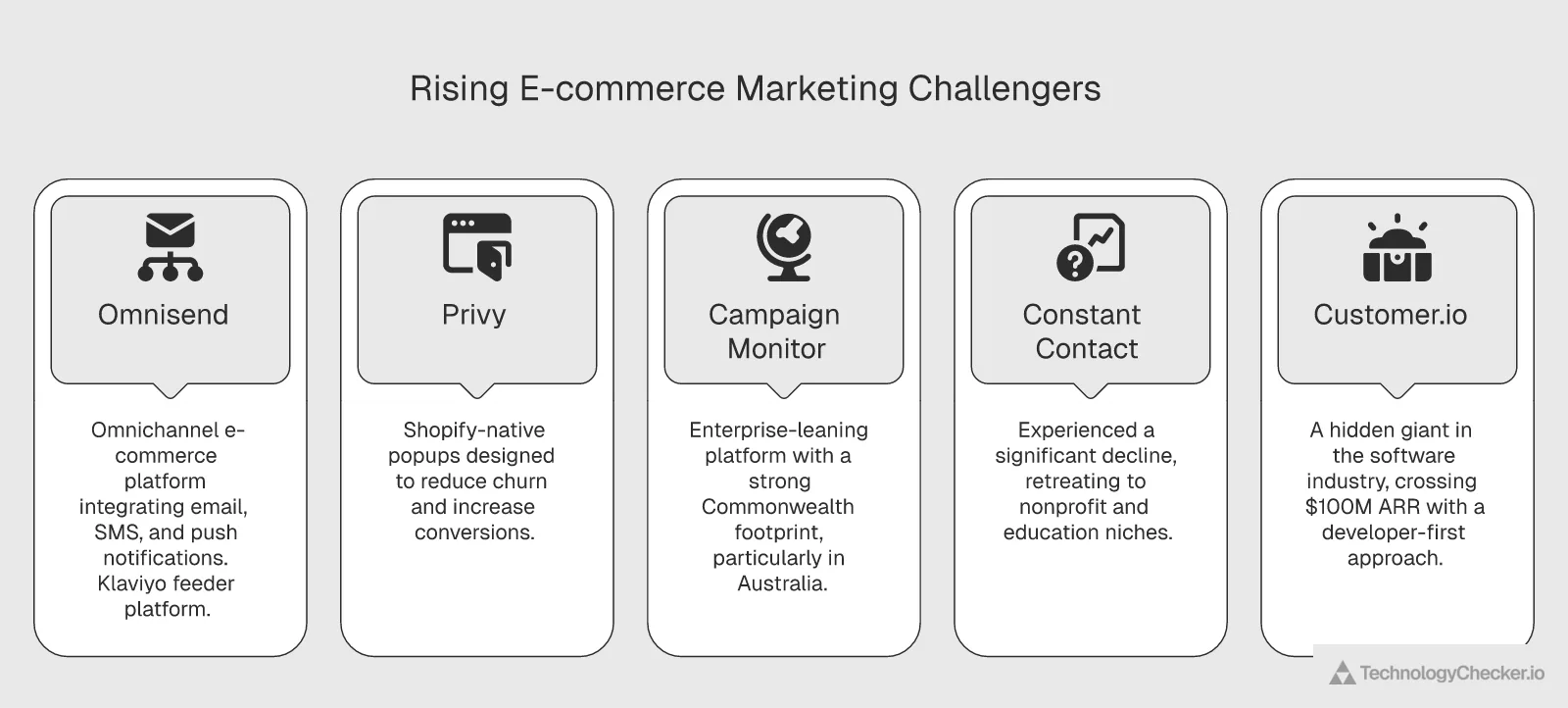

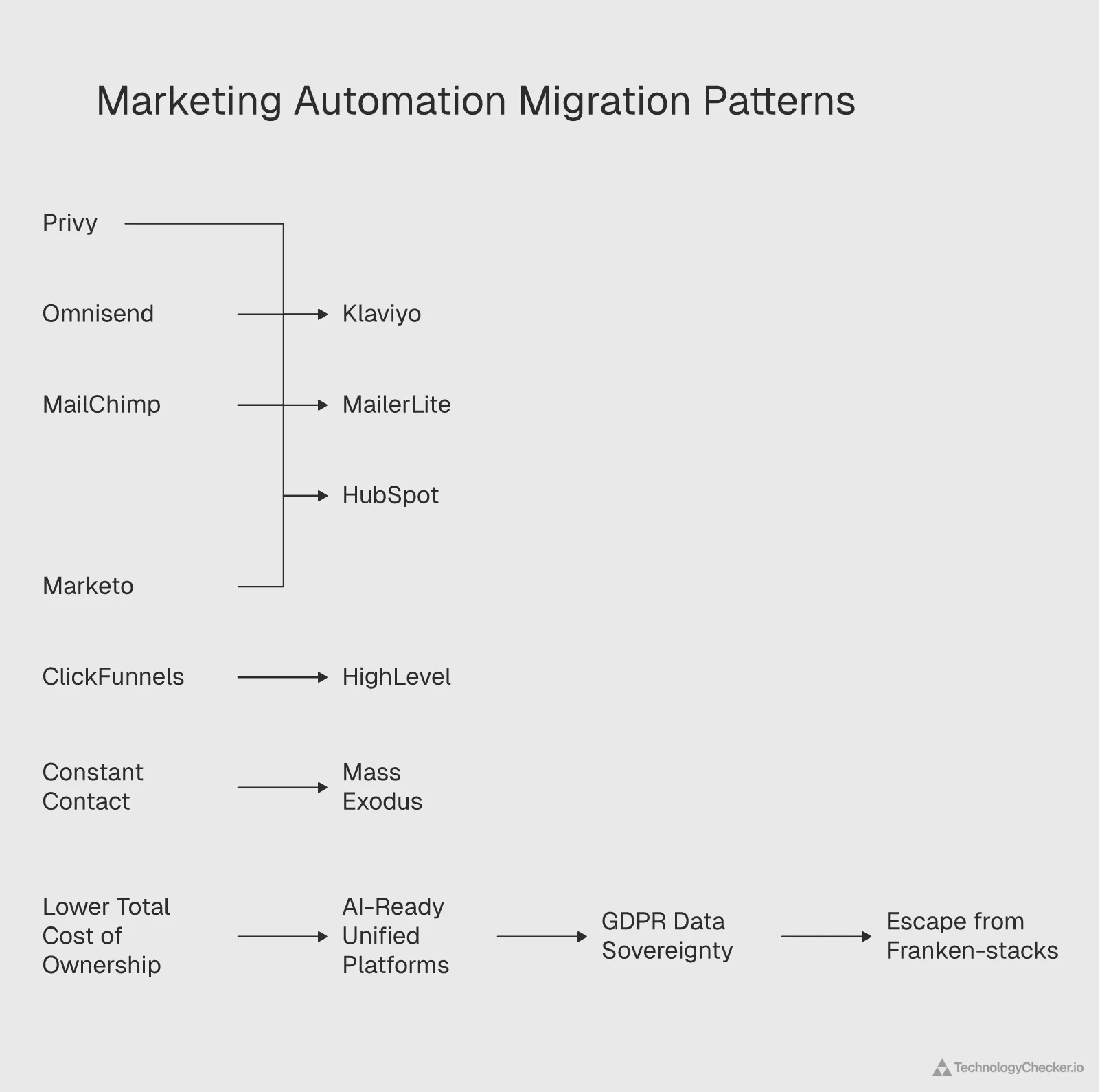

Omnisend (23,139 domains, Rank #14) — The omnichannel e-commerce specialist challenging Klaviyo's dominance with email + SMS + push notification bundles. For teams focused on push specifically, companies using OneSignal include Subway, GlaxoSmithKline, and S&P Global — OneSignal powers 12 billion messages daily across 29,900+ detected domains. Omnisend's user profile is strikingly similar to Klaviyo's: 15.65% retail and 10.29% fashion/apparel concentration. However, the migration data tells the competitive story—5,880 domains have switched from Omnisend to Klaviyo, while only 1,441 moved the other direction. Omnisend is effectively Klaviyo's primary feeder platform in the e-commerce space.

Mailmunch (22,003 domains, Rank #17) — A lead generation specialist combining opt-in forms, landing pages, and email marketing. What makes Mailmunch unique in our data is its 86.91% micro-business concentration (1-10 employees)—among the highest of any platform we track (second only to Kit's 93.9%). Its user base is heavily US-centric (51.3%) with a notable 3.4% Brazil presence, suggesting penetration into Latin American small business markets.

Privy (21,702 domains, Rank #18) — The Shopify-native popup and email platform shows the most dramatic previously-used count relative to active installations: 89,917 domains have previously used Privy versus only 21,702 currently active—a 4:1 churn ratio indicating significant market displacement. The destination? Klaviyo captured 7,073 former Privy users, making it the single largest migration path in our entire dataset for any platform pair.

Campaign Monitor (21,390 domains, Rank #19) — The Australian-born email platform tells a fascinating geographic story. Campaign Monitor has the strongest Commonwealth footprint of any platform: Australia accounts for 17.6% of its user base (vs. 5-8% for competitors), with the UK at 23.2%. Its 79.7% LinkedIn match rate is the second-highest we track (behind HubSpot's 82.2%), revealing a distinctly enterprise-leaning user base—Disney, Nokia, Bayer, Verizon, and Merck all appear in our company data. Campaign Monitor occupies a unique "premium email for agencies and enterprises" niche that no other mid-market platform serves.

Drip (7,372 domains, Rank #33) — The e-commerce automation purist that reports $1.5 billion+ in attributed revenue across its customer base. Founded in 2012 by Rob Walling and Derrick Reimer and acquired by Leadpages in 2016, Drip competes directly with Klaviyo in the Shopify/WooCommerce ecosystem but at a smaller scale. Our data shows over 80% of Drip users have 10 or fewer employees, and the platform's 47,635 previously-used domains (vs. 7,372 active) reveal a 6.5:1 churn ratio—many migrating to Klaviyo as they scale. Companies that use Drip include Trustpilot, Grafana Labs, and Social Media Examiner, suggesting the platform retains a following among technically-minded DTC and SaaS operators.

Constant Contact (7,028 domains, Rank #34) — The most dramatic decline story in our dataset. Founded in 1995 as Roving Software, Constant Contact was once a dominant email marketing platform—yet our data reveals 89,002 domains that previously used Constant Contact versus only 7,028 currently active, a staggering 12.7:1 churn ratio—the worst of any platform we track. Now independently operated under Clearlake Capital and Siris Capital, the platform has retreated into a nonprofit and education niche: 7.45% of its current users are nonprofits (highest concentration in the category), with companies that use Constant Contact including The World Bank, The Salvation Army, and Boston University. Its 82.1% LinkedIn match rate—nearly matching HubSpot—confirms these are formalized institutional users, not the small businesses that have long since migrated to MailChimp, Mailerlite, or Brevo.

GetResponse (6,196 domains, Rank #37) — Europe's bootstrapped success story. Founded in 1998 in Gdańsk, Poland by Simon Grabowski, GetResponse has grown to $150M in annual revenue and 350,000+ customers across 183 countries—all without raising a single dollar of outside funding. With 400 employees across 14 countries, the platform processes over 100 million emails daily and has won the MarTech Breakthrough Award for Best B2B Email Marketing Solution three years running (2023-2025). Companies that use GetResponse include Novo Nordisk, Red Bull, and Check Point Software, while the broader user base mirrors Brevo's European DNA: Poland and Central Europe are over-represented vs. US-centric competitors.

Customer.io (2,836 domains, Rank #55) — The highest-ARPU "hidden giant" in our data. With only 2,836 detected domain installations, Customer.io would seem like a minor player—until you learn it crossed $100M in annual recurring revenue in September 2025 (37% YoY growth), making it one of the most capital-efficient marketing automation companies ever built ($38.8M total funding). Over 34% of Customer.io users come from software and technology industries—the highest tech concentration in the category. Companies that use Customer.io include Seagate, The Economist, Apollo.io, Weight Watchers, and DataCamp. Its behavioral-first, event-driven architecture positions it as the "developer's marketing platform," explaining why domain-count detection dramatically understates its real footprint.

Part 5: Deep Dive—Company-Level Intelligence Across 17 Platforms

Here's where our data gets genuinely unique. Beyond detecting which platforms are installed, we've enriched our technology detection data with LinkedIn company profiles across all 17 marketing automation platforms in this report—over 500,000 enriched company records in total. This allows us to answer questions no other report can: Who exactly is using each platform?

The match rates alone tell a story:

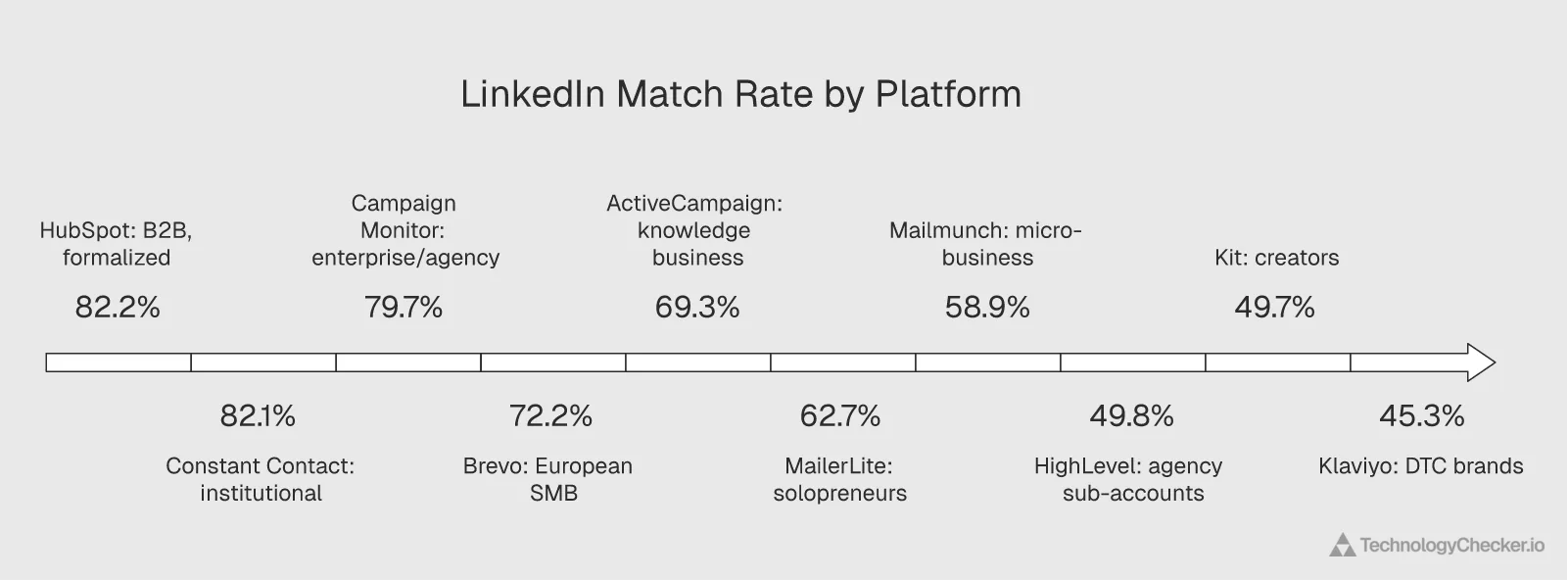

| Platform | Detected Domains | Enriched with Company Data | Match Rate |

|---|---|---|---|

| HubSpot | 121,300 | 99,700 | 82.2% |

| Constant Contact | 7,028 | 5,772 | 82.1% |

| Campaign Monitor | 21,390 | 17,053 | 79.7% |

| Brevo | 67,311 | 48,610 | 72.2% |

| ActiveCampaign | 56,932 | 39,448 | 69.3% |

| MailerLite | 95,861 | 60,139 | 62.7% |

| Mailmunch | 22,003 | 12,949 | 58.9% |

| Kit (ConvertKit) | 14,721 | 7,317 | 49.7% |

| HighLevel | 72,439 | 36,056 | 49.8% |

| GetResponse | 6,196 | 2,872 | 46.3% |

| Klaviyo | 147,491 | 66,837 | 45.3% |

| Omnisend | 23,139 | 10,188 | 44.0% |

| Customer.io | 2,836 | 1,236 | 43.6% |

| Drip | 7,372 | 3,173 | 43.0% |

| Privy | 21,702 | 9,291 | 42.8% |

| ClickFunnels | 29,755 | 8,789 | 29.5% |

| MailChimp | 283,090 | 74,778 | 26.4% |

Why match rates matter: An 82% match rate (HubSpot, Constant Contact) indicates formalized B2B companies or institutional organizations with established LinkedIn presence—businesses that care about professional visibility. Constant Contact's near-identical 82.1% rate is a surprise: it reveals that despite massive churn, its remaining users are overwhelmingly institutional (nonprofits, universities, healthcare systems). Campaign Monitor's 80% rate reveals a similarly enterprise-leaning user base. At the other end, ClickFunnels' 29.5% and MailChimp's 26.4% suggest solopreneurs and micro-businesses that often don't maintain LinkedIn company pages. The match rate itself is a powerful signal about user sophistication and formalization—the more "professional" the user base, the higher the match rate.

MailChimp: The SMB Generalist (283K Domains Analyzed)

The Profile: Based on companies using MailChimp we tracked, MailChimp remains the default choice for small businesses just getting started with email marketing.

| Attribute | MailChimp User Profile |

|---|---|

| Dominant Size | 1-10 employees (30%), 11-50 (25%), 51-200 (20%) |

| Top Industries | Retail (5.9%), Non-profits (3.6%), Wellness (2.5%), Advertising (2.5%) |

| Geographic Center | US (36%), UK (16%), Germany (11%), Canada (8%) |

| Median Founded | 2013 |

| Match Rate | 26.4% — lowest of any platform we track |

Key Insight: MailChimp's 26.4% LinkedIn match rate is the most revealing statistic in our data. It means nearly three-quarters of MailChimp domains belong to businesses too small or informal to maintain a LinkedIn company page—solo bloggers, Etsy sellers, church newsletters. Among the enriched sample, the 3.6% non-profit concentration is still the highest of any platform, confirming MailChimp's role as the de facto email tool for the third sector. The relatively balanced company size distribution in the enriched sample (30% micro / 25% small / 20% mid) suggests that when MailChimp does have formalized business users, they span the full spectrum.

Top Cities: London (3.2%), New York (1.2%), Los Angeles (0.8%), Toronto (0.7%), Paris (0.7%)

Klaviyo: The E-commerce Specialist (147K Domains Analyzed)

The Profile: According to our Klaviyo market share and usage data, Klaviyo has captured the direct-to-consumer market with surgical precision.

| Attribute | Klaviyo User Profile |

|---|---|

| Dominant Size | 1-10 employees (77%) |

| Top Industries | Retail (15.5%), Fashion/Apparel (10.8%), Wellness (4.3%), Food & Beverage (4.3%) |

| Geographic Center | US (54%), UK (13%), Australia (10.8%) |

| Median Founded | 2017 (youngest user base) |

| Match Rate | 45.3% — DTC brands often lack LinkedIn presence |

Key Insight: Klaviyo's 26% retail + fashion concentration is 4x higher than MailChimp's. These aren't just e-commerce companies—they're the DTC brands that emerged from the Shopify boom: skincare, supplements, athleisure, home goods. The 2017 median founding year confirms this is the platform of choice for pandemic-era DTC startups.

Australia over-indexes significantly (10.8% vs 7.2% for MailChimp)—reflecting the strong Shopify/DTC ecosystem in Sydney and Melbourne.

The DTC Vertical Stack:

- Personal Care Manufacturing: 2.8%

- Luxury Goods & Jewelry: 2.3%

- Food & Beverage Manufacturing: 1.7%

- Sporting Goods: 1.6%

HubSpot: The B2B Growth Engine (121K Domains Analyzed)

The Profile: Based on our HubSpot market share analysis, HubSpot has successfully moved upmarket while maintaining its growth-company DNA.

| Attribute | HubSpot User Profile |

|---|---|

| Dominant Size | 1-10 employees (53%), but 23% are 11-50 |

| 51+ employees | 19% (3x higher than competitors) |

| Top Industries | Software (8.5%), IT Services (6.6%), Advertising (5.7%), Business Consulting (4.9%) |

| Geographic Center | US (53%), UK (13%), Germany (8.8%) |

| Median Founded | 2015 |

| Match Rate | 82.2% — highest of any platform we track |

Key Insight: HubSpot's 15%+ tech/software concentration makes it the platform of B2B SaaS. The 82% LinkedIn match rate—highest of any platform—confirms these are formalized businesses with sales teams, marketing departments, and professional operations.

The Enterprise Signal: HubSpot has 3x the mid-market presence (51-200 employees: 13%) of any competitor. Its tiered pricing and CRM integration attract companies that have outgrown simple email tools but aren't ready for Salesforce complexity.

City Profile: San Francisco (1.1%) and Boston (0.5%) rank unusually high—these are the B2B tech hubs where HubSpot's inbound methodology originated.

HighLevel: The Agency Ecosystem (72K Domains Analyzed)

The Profile: Based on companies using HighLevel we analyzed, HighLevel has created something entirely new—a platform where agencies ARE the distribution channel.

| Attribute | HighLevel User Profile |

|---|---|

| Dominant Size | 1-10 employees (86%—highest of any platform) |

| Top Industries | Advertising Services (9.6%), Marketing Services (9.1%), Wellness (5.8%), Coaching (4.8%) |

| Geographic Center | US (73%—highest concentration) |

| Median Founded | 2018 (newest businesses) |

| Match Rate | 49.8% — many white-labeled agency sub-accounts |

Key Insight: The 19% combined agency + marketing services concentration tells the whole story. HighLevel isn't competing with MailChimp for end users—it's competing with white-label solutions for agencies. Those agencies then deploy it to thousands of local service businesses: dentists, roofers, gyms, real estate agents, chiropractors.

The Sun Belt Pattern: HighLevel's top US cities read like a map of America's fastest-growing metros:

- Miami (0.86%)

- Houston (0.83%)

- San Diego (0.65%)

- Dallas (0.61%)

- Las Vegas (0.56%)

- Tampa (0.51%)

- Phoenix (0.46%)

These aren't tech hubs—they're local service business hubs where construction, real estate, and medical practices are booming.

The Solopreneur Signal: HighLevel's 22% self-owned/self-employed rate (vs 14% for others) reflects its target market: individual agency owners and local business operators who need all-in-one solutions.

ActiveCampaign: The Course Creator's Choice (57K Domains Analyzed)

The Profile: Based on our ActiveCampaign market share analysis, ActiveCampaign has carved out a unique niche as the platform for educators, coaches, and info-product creators.

| Attribute | ActiveCampaign User Profile |

|---|---|

| Dominant Size | 1-10 employees (73%), 11-50 (17%) |

| Top Industries | Training & Coaching (6.2%), Advertising (5.9%), Business Consulting (4.5%), Software (3.4%) |

| Geographic Center | US (33%), France (14%), Netherlands (13%) |

| Median Founded | 2014 |

| Match Rate | 69.3% — formalized knowledge businesses |

Key Insight: ActiveCampaign's 6.2% professional training/coaching concentration is 2-3x higher than any competitor. Combined with business consulting (4.5%) and software (3.4%), this is clearly the platform of choice for the knowledge economy: course creators, membership site operators, coaching businesses.

The European Anomaly: ActiveCampaign has the most geographically diverse user base of any platform. The 13% Netherlands and 14% France concentrations are extraordinary—this is where European coaching and online education markets have standardized on ActiveCampaign's automation workflows.

Top Cities: Amsterdam (0.88%) and Copenhagen (0.39%) appear prominently—both are hubs for the European coaching and personal development industry.

Brevo (Sendinblue): Europe's Default (67K Domains Analyzed)

The Profile: According to our Brevo market share and usage data, Brevo has become the GDPR-native alternative for European businesses who want to keep data local.

| Attribute | Brevo User Profile |

|---|---|

| Dominant Size | 1-10 employees (70%), but 18% at 11-50 |

| Top Industries | Retail (4.9%), IT Services (4.4%), Software (4.1%), Advertising (3.9%) |

| Geographic Center | France (30%), US (20%), Germany (11%) |

| Median Founded | 2014 |

| Match Rate | 72.2% — formalized European businesses |

Key Insight: Brevo's 30% France concentration and Paris headquarters make it the obvious choice for French businesses. Combined with Germany (11%) and Italy (6.6%), nearly half of Brevo's user base is continental European. European public sector organizations choose Brevo for data sovereignty.

The Tourism Connection: Brevo shows notably strong presence in travel (1.2%) and hospitality (1.3%)—the European tourism industry has standardized on local email providers.

City Concentration: Paris alone accounts for 4.4% of all Brevo users—the highest single-city concentration of any platform we track.

MailerLite: The Solopreneur's Secret Weapon (96K Domains Analyzed)

The Profile: According to our MailerLite market share and usage data, MailerLite has built one of the largest user bases in marketing automation while flying under the radar of most industry reports.

| Attribute | MailerLite User Profile |

|---|---|

| Dominant Size | 1-10 employees (83%) |

| Top Industries | Training & Coaching (5.1%), Business Consulting (4.8%), Advertising (4.6%) |

| Geographic Center | US (36%), UK (18%), Poland (9.1%) |

| Company Type | Predominantly solopreneurs and small content businesses |

Key Insight: MailerLite's 9.1% Poland concentration is the standout geographic signal—no other platform has more than 2% penetration in Poland. This Baltic/CEE footprint (MailerLite was founded in Lithuania) represents a genuine regional competitive moat. Combined with 5.6% Netherlands, MailerLite has become the default email platform for Central and Northern European solopreneurs.

The MailChimp Replacement Signal: Our migration data shows 5,980 domains switching from MailChimp to MailerLite—the third-largest migration flow from MailChimp after Klaviyo (16,976) and HubSpot (7,912). With only 1,512 going in the reverse direction, MailerLite achieves a 4:1 net migration ratio from MailChimp, making it one of the most effective MailChimp replacement platforms in our data.

ClickFunnels: The Solopreneur's Funnel Machine (30K Domains Analyzed)

The Profile: Based on companies using ClickFunnels we tracked, ClickFunnels dominates the "funnel builder" sub-category with a user base that mirrors HighLevel's solopreneur focus but with a coaching/info-product flavor.

| Attribute | ClickFunnels User Profile |

|---|---|

| Dominant Size | 1-10 employees (81%) |

| Top Industries | Advertising Services, Coaching & Wellness, Education |

| Geographic Center | US-dominated, with India and Australia as secondary markets |

| Revenue | $265.3M in 2023, 150K+ active customers |

| Match Rate | 29.5% — second-lowest, reflecting solopreneur dominance |

Key Insight: ClickFunnels' 29.5% LinkedIn match rate—second only to MailChimp's 26.4%—confirms its user base is overwhelmingly informal: individual coaches, consultants, and "Funnel Hackers" who don't maintain LinkedIn company pages. The 46,521 previously-used domains signal intensifying competition from HighLevel and Kajabi, both of which offer funnel capabilities alongside broader CRM and automation features. ClickFunnels commands 55.8% of the sales funnel software market but faces dilution risk as it expands into general-purpose website building with ClickFunnels 2.0.

Kit (ConvertKit): The Pure Creator Platform (15K Domains Analyzed)

The Profile: According to our Kit (ConvertKit) market share data, Kit has built the most concentrated micro-business user base in the entire marketing automation category.

| Attribute | Kit User Profile |

|---|---|

| Dominant Size | 1-10 employees (93.9%—highest of any platform) |

| Top Industries | Blogging, Podcasting, Online Courses, Coaching |

| Geographic Center | US-centric, 55+ countries |

| Customer Base | 600,000+ creators, $400M+ in creator earnings |

| Match Rate | 49.7% — half of creators don't maintain LinkedIn pages |

Key Insight: Kit's 93.9% micro-business concentration is the highest of any platform we track—even higher than HighLevel (86%) and MailerLite (83%). This isn't a bug; it's the product. Kit was built from day one for individual creators, not businesses. The October 2024 rebrand from ConvertKit to Kit reflects ambitions to become a full creator operating system (commerce, recommendations, audience-building), positioning it in the $250 billion creator economy. With a free tier offering up to 10,000 subscribers, Kit has become the standard "first email tool" for creators who later graduate to ActiveCampaign or Klaviyo as they build commerce operations.

Constant Contact: The Institutional Survivor (7K Domains Analyzed)

The Profile: According to companies using Constant Contact in our database, Constant Contact has undergone the most dramatic repositioning in our data—from mass-market email leader to institutional niche player.

| Attribute | Constant Contact User Profile |

|---|---|

| Dominant Sectors | Nonprofits (7.45%), Education, Healthcare |

| Notable Clients | The World Bank, Salvation Army, Boston University, UT Southwestern Medical Center |

| Geographic Center | Heavily US-centric |

| Founded | 1995 (oldest platform in our dataset) |

| Match Rate | 82.1% — near-identical to HubSpot, revealing institutional users |

Key Insight: The 12.7:1 churn ratio (89,002 previously-used domains vs. 7,028 active) tells the entire Constant Contact story. This is a platform that was once ubiquitous among small businesses but has been systematically displaced by MailChimp, MailerLite, and Brevo over the past decade. What remains is a hardened institutional core: nonprofits, universities, and healthcare systems that chose Constant Contact 10-15 years ago and have no organizational appetite for migration. The 82.1% LinkedIn match rate—matching HubSpot—confirms these are not small businesses; they're formalized organizations with compliance requirements and long procurement cycles. Constant Contact has become, inadvertently, an enterprise nonprofit email platform.

Customer.io: The Developer's Marketing Platform (3K Domains Analyzed)

The Profile: Based on our Customer.io market share data, Customer.io is the most capital-efficient company in the marketing automation space—and its domain-count detection dramatically understates its real market impact.

| Attribute | Customer.io User Profile |

|---|---|

| Dominant Industries | Software Development (34%+), IT Services, SaaS |

| Notable Clients | Seagate, The Economist, Apollo.io, Weight Watchers, DataCamp, TryHackMe |

| ARR | $100M+ ARR (crossed Sep 2025), 37% YoY growth |

| Capital Efficiency | $100M ARR on only $38.8M total funding |

| Match Rate | 43.6% — tech companies, many bootstrapped/early-stage |

Key Insight: Customer.io's $100M ARR on just 2,836 detected domains implies an average revenue per detected domain of ~$35,000/year—roughly 100x higher than MailChimp's implied ARPU. This makes sense: Customer.io's event-driven, behavioral messaging architecture serves product-led growth companies that send millions of transactional and lifecycle messages through server-side integrations that our web crawlers may not detect. It's the "HubSpot of product-led growth," per Sacra's analysis—invisible in domain counts, dominant in developer mindshare.

Cross-Platform Insights: What the Data Reveals

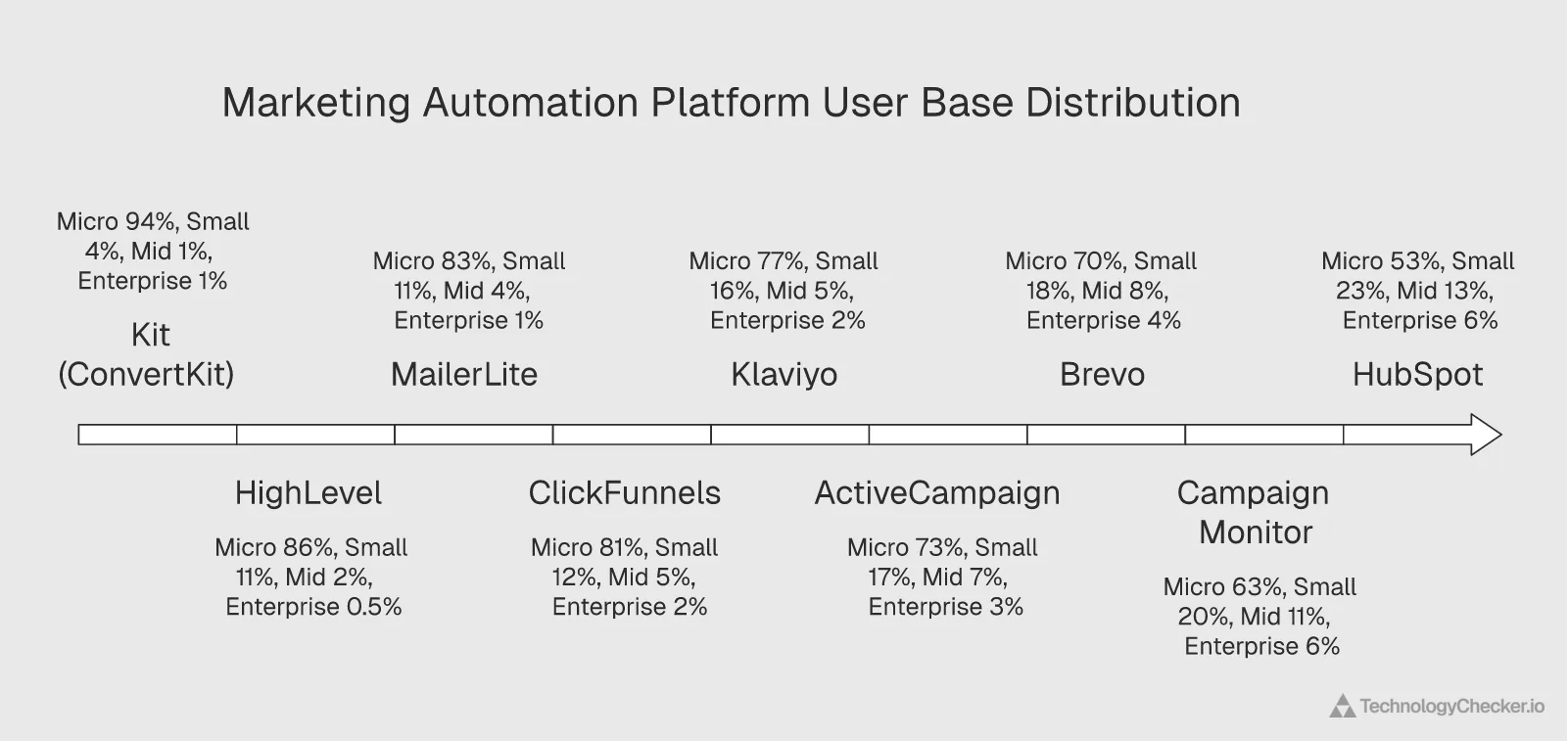

1. Company Size Reveals Platform Positioning

| Platform | Micro (1-10) | Small (11-50) | Mid (51-200) | Enterprise (201+) |

|---|---|---|---|---|

| Kit (ConvertKit) | 94% | 4% | 1% | 1% |

| HighLevel | 86% | 11% | 2% | 0.5% |

| MailerLite | 83% | 11% | 4% | 1% |

| ClickFunnels | 81% | 12% | 5% | 2% |

| Drip | 80% | 13% | 5% | 2% |

| Klaviyo | 77% | 16% | 5% | 2% |

| ActiveCampaign | 73% | 17% | 7% | 3% |

| Brevo | 70% | 18% | 8% | 4% |

| Campaign Monitor | 63% | 20% | 11% | 6% |

| HubSpot | 53% | 23% | 13% | 6% |

Kit's 94% micro-business concentration is the most extreme in our data—nearly every Kit user is a solo creator. HubSpot's mid-market dominance is clear at the other end. ClickFunnels (81%) and Drip (80%) cluster with HighLevel and MailerLite in the solopreneur tier. Campaign Monitor, despite its smaller overall footprint, has a notably enterprise-leaning profile—31% of its users have 11+ employees, second only to HubSpot. Constant Contact (not shown due to small sample) has a similarly institutional profile, with its 82.1% match rate suggesting formalized organizations.

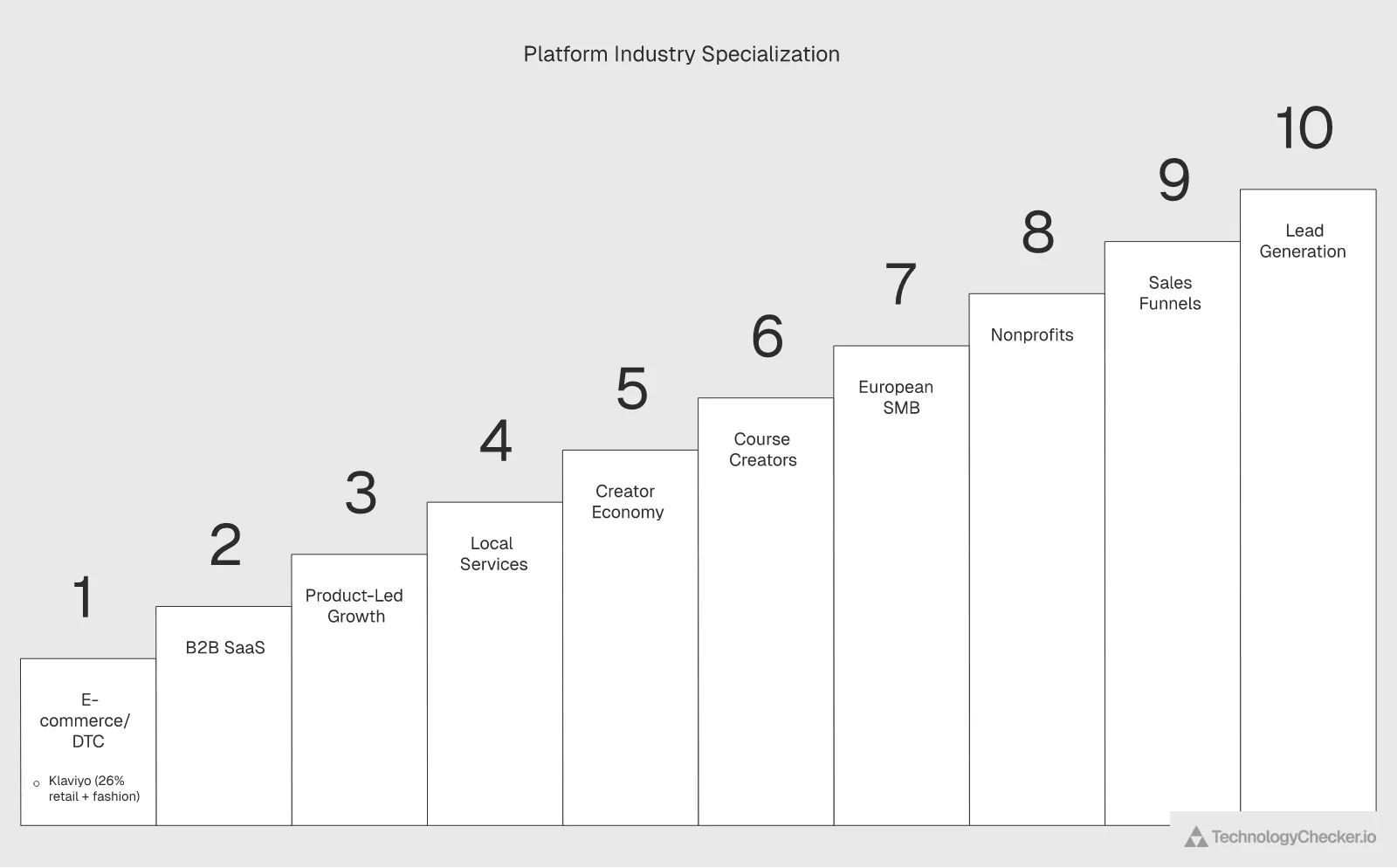

2. Industry Concentration Defines Use Case

| Use Case | Platform | Key Industry Concentration |

|---|---|---|

| E-commerce/DTC | Klaviyo | 26% Retail + Fashion |

| E-commerce (Budget) | Omnisend | 26% Retail + Fashion |

| B2B SaaS | HubSpot | 15% Software + IT |

| Product-Led Growth | Customer.io | 34% Software + Tech |

| Local Services | HighLevel | 19% Agencies + Marketing Services |

| Sales Funnels/Coaching | ClickFunnels | Coaching, Wellness, Advertising |

| Creator Economy | Kit (ConvertKit) | Bloggers, Podcasters, Course Creators |

| Content Creators | MailerLite | 10% Training + Consulting |

| Course Creators | ActiveCampaign | 6% Training + E-Learning |

| Non-profits/Institutions | Constant Contact | 7.45% Non-profit, Education, Healthcare |

| Non-profits (Mass Market) | MailChimp | 3.6% Non-profit |

| European SMB | Brevo | 30% France, GDPR-native |

| European Bootstrapped | GetResponse | Poland + Central Europe, Enterprise clients |

| Shopify Popups | Privy | 33% Retail + Fashion |

| E-commerce (DTC Purist) | Drip | Shopify/WooCommerce micro-brands |

| Agencies/Enterprise Email | Campaign Monitor | 4% Advertising + 3% Non-profits |

3. Geographic Patterns Reveal Market Strategy

| Platform | US Concentration | Europe Concentration | Key Non-US Market |

|---|---|---|---|

| HighLevel | 73% | 9% | Canada (7%) |

| Klaviyo | 54% | 16% | Australia (11%) |

| Privy | 53% | 10% | Brazil (15%) |

| Mailmunch | 51% | 12% | Canada (7%) |

| Omnisend | 49% | 19% | Australia (8%) |

| HubSpot | 53% | 22% | Germany (9%) |

| MailerLite | 36% | 33% | Poland (9%) |

| MailChimp | 36% | 27% | UK (16%) |

| ActiveCampaign | 33% | 32% | Netherlands (13%) |

| Campaign Monitor | 31% | 28% | Australia (18%) |

| Brevo | 20% | 48% | France (30%) |

4. Company Age Signals Market Maturity

| Platform | Median Founded | Interpretation |

|---|---|---|

| HighLevel | 2018 | New agencies, new local businesses |

| Klaviyo | 2017 | DTC boom generation |

| MailerLite | 2016 | Digital-native solopreneurs |

| HubSpot | 2015 | Growth-stage companies |

| ActiveCampaign | 2014 | Established knowledge businesses |

| Brevo | 2014 | Mature European SMBs |

| MailChimp | 2013 | Legacy small businesses |

| Campaign Monitor | 2010 | Established enterprises and agencies |

Part 6: Industry-Specific Patterns and Case Studies

Healthcare: The Patient Engagement Revolution

Healthcare domains show distinctive patterns in our crawls. The sector has moved beyond simple appointment reminders to comprehensive "Patient Journey Management," driven by the need to improve outcomes while navigating strict regulatory frameworks.

Case Study: Oscar Health – Personalized Member Outreach

Oscar Health adopted a "hackathon" culture toward Generative AI, developing 47 insurance-specific Large Language Models. According to Oscar's AI strategy documentation and Digital Insurer analysis, they utilized their proprietary "Campaign Builder" platform to run rigorous experiments on messaging effectiveness.

The AI models analyzed member health profiles to generate highly specific outreach campaigns, introducing dynamic "action items" on mobile app home screens. This data-driven approach led to significant improvements in Net Promoter Score (NPS) and Medical Loss Ratio (MLR)—proving that automation drives both satisfaction and profitability (Oscar Tech Blog).

Case Study: Doctolib (France) – Scaling Access to Care

Doctolib, managing 500 million appointments annually, leveraged Microsoft Azure AI and massive SMS automation infrastructure (25 million messages/month). According to smsmode case study and Microsoft's AI success stories, their AI Consultation Assistant transcribes patient visits in real-time and generates structured medical summaries.

Results: Clinicians reported 2x increase in face-to-face patient time, while automated SMS drastically reduced no-show rates.

E-commerce: Agentic Commerce

Case Study: Tatcha – The "Fukubukuro" Strategy

Tatcha utilized Klaviyo's sophisticated segmentation for their annual New Year promotion. According to Klaviyo's case study, they moved from batch-and-blast tactics to "Category Affinity" targeting—identifying less-engaged subscribers who had previously purchased featured product categories.

Using "Smart Sending" features for frequency management, the strategy delivered 20% year-over-year revenue growth for the promotion, demonstrating that precise segmentation allows brands to safely market to "dormant" users when content is highly relevant.

Case Study: Sesame Care – Closing the Loop

Sesame Care implemented Braze for engagement and Segment (CDP) for data unification to convert visitors who didn't transact on first visit. According to Braze's case study, they created a "nurture layer" tracking specific behavioral events to guide users back to booking.

Result: The new stack successfully converted "window shoppers" into patients, creating sustainable revenue streams outside expensive paid search acquisition.

B2B/SaaS: Account-Based Orchestration

B2B domains reveal evolution from lead generation (volume) to account-based orchestration (precision). According to The Smarketers' 2026 trends analysis, AI tools now identify entire "buying committees" within target accounts, serving distinct content streams to each role.

Platforms like Monday.com CRM enable shared dashboards ensuring marketing "warm-up" activities and sales outreach are perfectly synchronized.

Part 7: The Enterprise Battle—HubSpot vs. Salesforce

The rivalry between HubSpot and Salesforce has intensified, reshaping the mid-market and enterprise segments.

HubSpot's Up-Market March

HubSpot has successfully shed its "SMB-only" reputation. With the launch of Breeze AI and advanced Workspaces, it now offers governance and power required by large organizations while retaining signature usability (HubSpot Spring 2025 Spotlight).

According to Cometly's platform comparison, HubSpot has become a prime destination for companies migrating away from complex legacy systems.

Salesforce's Agentic Defense

Salesforce retains dominance in complex, multinational deployments through Agentforce—allowing enterprises to deploy autonomous service and sales agents within the Salesforce ecosystem. According to SalesHive's comparison, Salesforce's data gravity remains unmatched for organizations requiring extreme customization.

However, Pixel Consulting's analysis notes that for organizations not requiring such complexity, Salesforce increasingly appears to have high "Total Cost of Ownership" compared to nimbler rivals.

Part 8: Migration and Modernization Patterns

The "Marketo to HubSpot" Wave

Market intelligence indicates significant migration from Adobe Marketo to HubSpot's Marketing Hub Enterprise. According to Aptitude 8:

- Operational Drag: Legacy platforms require specialized technical staff for basic campaigns; HubSpot's "product-first" design lets marketers execute without engineering support

- Total Cost of Ownership: Marketo pricing can range from $960 to over $7,000/month with add-ons; HubSpot offers transparent pricing and lower implementation costs (Envy Blog Migration Guide)

- Feature Parity: With "Breeze" AI agents and enterprise governance tools, HubSpot has closed the feature gap

Unifying Data on Salesforce Data Cloud

For global enterprises where Salesforce is the system of record, migration is internal—moving disparate data sources into Salesforce Data Cloud. According to 360 Degree Cloud, this enables "Identity Resolution" at scale, creating the foundation for Agentforce.

Scandiweb's case study documents how a luxury fashion house unified customer profiles across boutiques and online stores, enabling stylists to provide recommendations based on clients' online browsing history.

Part 9: ROI, Budgeting, and the New Metrics

Budget Trends: Efficiency Over Volume

Marketing budgets in 2026 reflect a "consolidate and conquer" strategy. Gartner data shows martech now commands 23.8% of total marketing budgets — nearly matching paid media at 27.9% — as detailed in our marketing technology statistics roundup. According to Neil Patel's budget analysis, CFOs are scrutinizing tech stacks, demanding elimination of redundant tools. "Spray and pray" tactics are being defunded in favor of channels with defensible, attributable ROI.

As AI agents automate content distribution, the marginal cost of sending messages drops to near zero. Consequently, value shifts to creating high-quality, distinctive content. Budgets are reallocating from ad spend to creative production (Digital Marketing Institute Trends).

The Return on Automation

Industry benchmarks suggest compelling economics:

- $5.44 return for every dollar invested in marketing automation (Cropink Statistics)

- 2,000% ROI achieved by businesses implementing behavioral triggers (ActiveCampaign via Enricher.io)

- 30% of revenue generated through automated flows for optimized e-commerce brands

New Success Metrics

The KPIs of 2026 have evolved to measure autonomy effectiveness:

- Return on Automation (ROA): Financial yield per automation dollar

- Velocity Metrics: Lead velocity and time-to-close rather than lead volume

- Agent Performance: Human intervention rate and tasks-per-agent measuring operational leverage

Part 10: Future Outlook—Invisible Marketing (2027-2030)

As we look beyond 2026, the trajectory points toward Invisible Marketing—where technology disappears into seamless customer experience.

According to KEO Marketing's AI guide and Brands at Play's trend analysis:

Autonomous Budget Allocation: By 2028, AI agents will likely control majority of media buying—dynamically shifting budgets between channels based on real-time ROAS without requiring human sign-off for adjustments.

The End of the Dashboard: The "Conversational UI" will replace complex analytics dashboards. Marketers will simply ask systems for insights, receiving instant natural-language reports.

Governance as Primary Role: As agents take over execution, human marketers will shift to setting ethical guardrails, brand voice guidelines, and strategic objectives within which AI operates (Improvado AI Guide).

Part 11: Key Strategic Insights

After analyzing 30 million domains and synthesizing industry research, several strategic insights emerge:

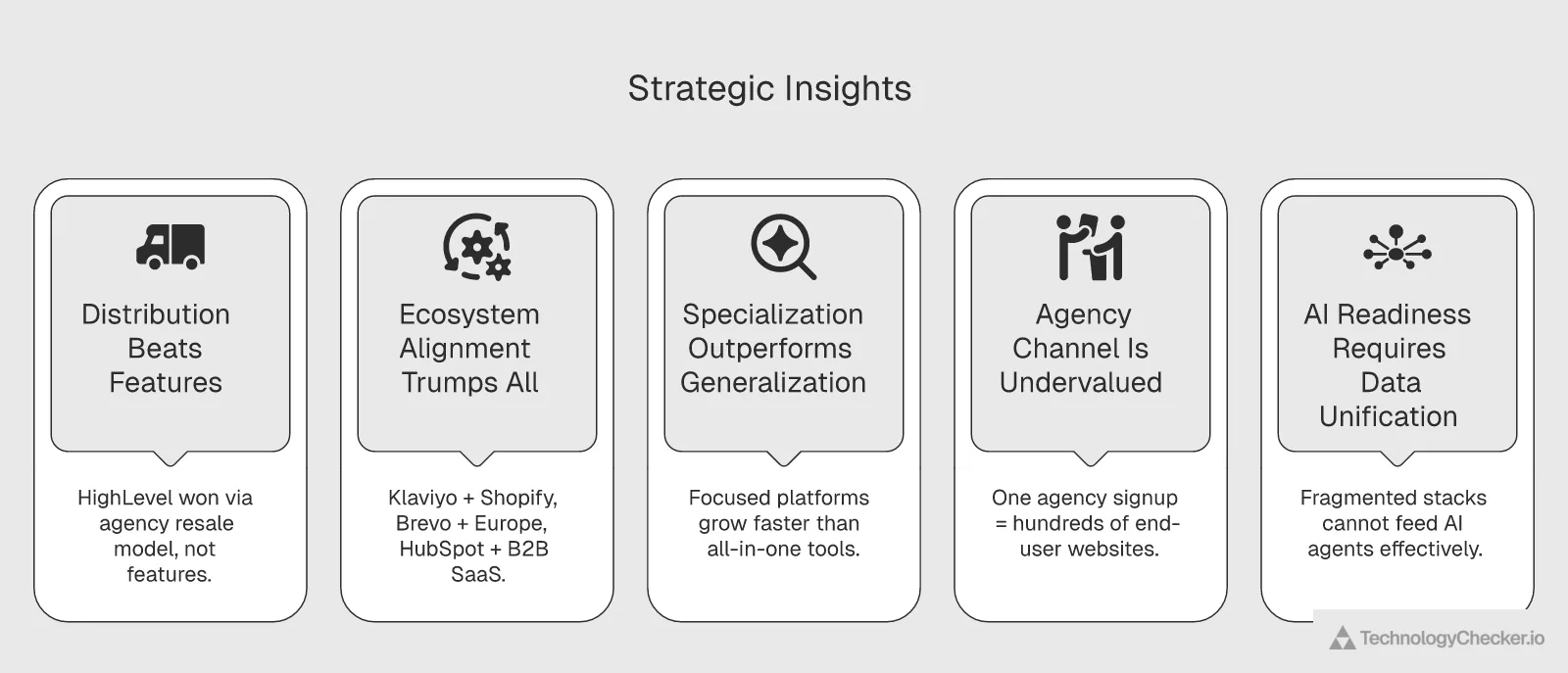

1. Distribution Model Innovation Beats Feature Competition

HighLevel didn't win on features—it won by creating a distribution model reaching businesses traditional software sales cannot. The lesson: how you deliver software matters as much as what it does.

2. Ecosystem Alignment Trumps Everything

Klaviyo's dominance in e-commerce, Brevo's strength in Europe, HubSpot's traction among scaling startups, MailerLite's penetration in Central European creator communities—each platform's success correlates with deep ecosystem integration, not feature comparison charts.

3. Specialization Outperforms Generalization

The fastest-growing platforms in our data (Klaviyo, HighLevel, MailerLite) have the clearest positioning. Even among smaller platforms, the pattern holds: Omnisend and Privy grow by targeting e-commerce exclusively, Kit owns the creator economy, Customer.io dominates product-led growth, while Campaign Monitor retains enterprise clients through agency-first positioning. The cautionary tale is Constant Contact: once a mass-market leader, its attempt to serve everyone resulted in a 12.7:1 churn ratio—the sharpest decline in our dataset. MailChimp's attempt to become everything to everyone hasn't prevented growth, but it's grown slower than focused competitors.

4. The Agency Channel Is Undervalued

HighLevel's success demonstrates that agencies function as highly effective distribution channels. For the SMB market, "managed service" may prove more sustainable than "self-service."

5. AI Readiness Requires Data Unification

Organizations successfully deploying agent-based automation have completed data unification projects. Fragmented stacks can't feed AI systems effectively—expect continued migration toward unified platforms. Our guide on finding companies by technology stack shows how sales teams use this migration signal for targeted prospecting.

6. Brand Is the Ultimate Ranking Factor

According to Insider One's best practices guide, successful automation builds brand value that algorithms must recognize. Every click is a vote; user experience has become direct ranking input.

Methodology

This report draws on TechnologyChecker.io's proprietary technology detection infrastructure combined with industry research. For a broader look at how the technology intelligence industry is evolving, see our comprehensive market overview.

Primary Data Source: Monthly crawls across 29.9 million active domains, detecting technology installations through HTTP headers, JavaScript libraries, DNS records, and HTML patterns.

Platforms Analyzed:

| Platform | Detection Method |

|---|---|

| MailChimp | JavaScript embed, form patterns |

| Klaviyo | JavaScript SDK, API calls |

| HubSpot | Tracking code, forms |

| MailerLite | JavaScript tracking, embedded forms |

| HighLevel | Tracking scripts, widgets |

| Brevo | JavaScript tracking |

| ActiveCampaign | Form embeds, tracking |

| ClickFunnels | Funnel scripts, page patterns |

| Kit (ConvertKit) | JavaScript tracking, form embeds |

| Omnisend | JavaScript SDK, tracking pixels |

| Mailmunch | Form embeds, popup scripts |

| Privy | JavaScript widget, popup patterns |

| Campaign Monitor | JavaScript embed, form patterns |

| Drip | JavaScript SDK, tracking scripts |

| Constant Contact | Form embeds, tracking pixels |

| GetResponse | JavaScript tracking, form patterns |

| Customer.io | JavaScript SDK, event tracking |

Detection Accuracy: 95% accuracy across 20,000+ tracked technologies, validated against known implementations.

Secondary Sources: Industry reports from Fortune Business Insights, Grand View Research, Mordor Intelligence, Sacra, BuiltWith Trends, and platform-specific case studies.

Historical Data: 20-year historical trend data enables longitudinal analysis of technology adoption patterns.

Limitations: Data reflects detectable web installations only. Mobile apps, server-side implementations, and custom domains may reduce detection accuracy for some deployments.

Conclusion: What This Means for Your Strategy

The marketing automation landscape has transformed from MailChimp's near-monopoly in 2015 to a diverse, competitive ecosystem in 2026. The winners share common characteristics: clear positioning, ecosystem alignment, innovative distribution, and AI-ready architecture.

For marketers evaluating platforms, the data suggests focusing less on feature comparisons and more on:

- Ecosystem fit: Does the platform integrate deeply with your core systems?

- Distribution alignment: Does the vendor's sales model match your buying preferences?

- Data architecture: Can the platform support agent-based automation as it matures?

- Specialization: Does the platform focus on your specific use case or try to serve everyone?

The platforms dominating our detection data aren't necessarily those with the longest feature lists—they're the ones that have made intentional choices about who they serve and how they deliver value. Explore the detailed adoption data, company profiles, and migration patterns for each platform: MailChimp, Klaviyo, HubSpot, MailerLite, HighLevel, Brevo, ActiveCampaign, ClickFunnels, Kit (ConvertKit), Omnisend, Mailmunch, Privy, Campaign Monitor, Drip, Constant Contact, GetResponse, and Customer.io.

References

- Fortune Business Insights - Marketing Automation Software Market: https://www.fortunebusinessinsights.com/marketing-automation-software-market-108852

- Grand View Research - Marketing Automation Market Analysis: https://www.grandviewresearch.com/industry-analysis/marketing-automation-software-market

- Mordor Intelligence - Marketing Automation Software Market: https://www.mordorintelligence.com/industry-reports/global-marketing-automation-software-market-industry

- The Business Research Company - Marketing Automation Report: https://www.thebusinessresearchcompany.com/report/marketing-automation-global-market-report

- Cropink - Marketing Automation Statistics: https://cropink.com/marketing-automation-statistics

- Birdeye - Enterprise Marketing Automation Tools: https://birdeye.com/blog/marketing-automation-tools/

- ClickFunnels Revenue & Customer Data (Latka): https://getlatka.com/companies/clickfunnels

- ConvertKit Rebrands to Kit (BusinessWire): https://www.businesswire.com/news/home/20241001564521/en/ConvertKit-Rebrands-to-Kit-Pioneering-a-New-Era-for-the-Creator-Economy-and-Email

- Customer.io Crosses $100M ARR: https://customer.io/learn/announcements/customerio-crossed-100m-note-from-ceo

- Customer.io - The HubSpot of Product-Led Growth (Sacra): https://sacra.com/research/customer-io-the-hubspot-of-product-led-growth/

- GetResponse Bootstrapped Success (Tech.eu): https://tech.eu/2016/09/26/poland-getresponse

- GetResponse Revenue Data (Latka): https://getlatka.com/companies/getresponse

This analysis is powered by TechnologyChecker.io's technology detection platform, which provides real-time technology profiles, verified contacts, and 20-year historical data across 29.9 million active domains. For custom technographic analysis or API access, visit technologychecker.io.

About the Author

Mehmet Suleyman is the CEO & Co-founder of TechnologyChecker.io, where he drives innovation in technographic intelligence. With expertise in web crawling, data analytics, and AI-driven insights, Mehmet leads a platform delivering 95% detection accuracy across 20,000+ technologies. He holds an M.Sc. in Data Science and Artificial Intelligence from Middle East Technical University and certifications including AWS Solutions Architect and Google Cloud Professional Data Engineer.

Connect with Mehmet on LinkedIn | Follow TechnologyChecker.io for weekly technology adoption insights.

CEO & Co-founder

12+ years of experience

Mehmet is the CEO and co-founder of TechnologyChecker.

- BSc Computer Engineering, Bilkent University

- Certified SaaS Growth Strategist

- Member, British Computer Society (BCS)

Never miss our research